Who Gets the House in a Los Angeles Divorce? Understanding the Moore-Marsden Formula

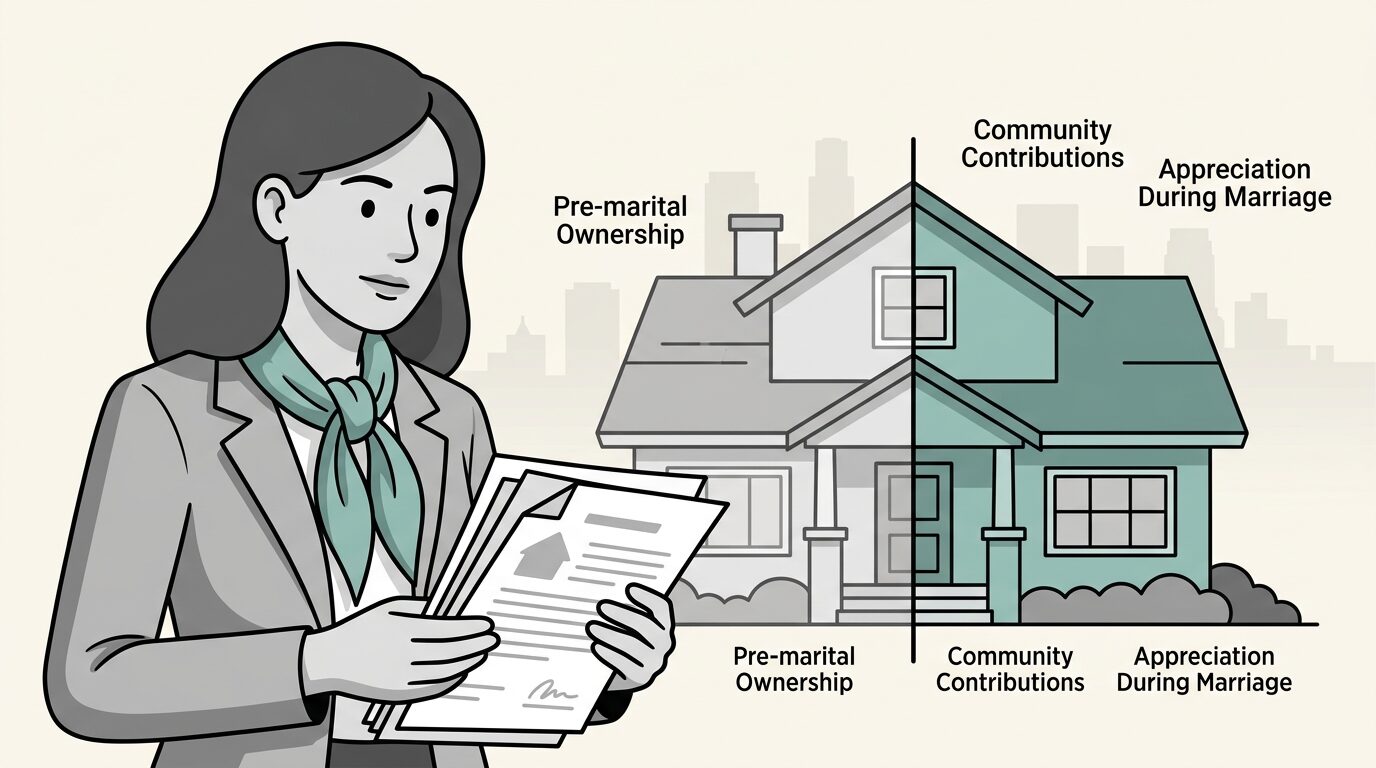

When one spouse buys a home before marriage and both contribute to it during the marriage, determining who gets what in a divorce becomes complicated. California law addresses this through the Moore-Marsden formula, a calculation that determines how much of a home’s equity belongs to each spouse. In Los Angeles, where property values routinely reach seven figures, understanding this formula is essential for anyone facing divorce with a home purchased before marriage.

What is the Moore-Marsden formula and when does it apply?

The Moore-Marsden formula is a California legal calculation that determines how much of a home’s equity is community property versus separate property when one spouse purchased the home before marriage but community funds were used to pay the mortgage during the marriage.

The formula originates from two landmark California cases: In re Marriage of Moore (1980) and In re Marriage of Marsden (1982). These cases established how courts should divide equity in homes where a down payment was made before marriage but mortgage payments were paid with community funds.

For the Moore-Marsden formula to apply, three conditions must be met:

- One spouse purchased the property before marriage (title remains in that person’s name)

- Community funds paid down the mortgage principal during the marriage

- The property appreciated in value during the marriage

Only principal payments count toward the calculation. Interest, property taxes, and insurance payments do not factor into the formula, even if paid with community income.

The formula becomes especially relevant in complex property division scenarios where significant assets are at stake. In 2025, the California Court of Appeal issued In re Marriage of Freeman, which clarified important timing rules for valuation. The court confirmed that while the community’s percentage interest is fixed as of the date of separation, the actual property valuation for division purposes occurs at or near the time of trial.

How does the Moore-Marsden calculation actually work?

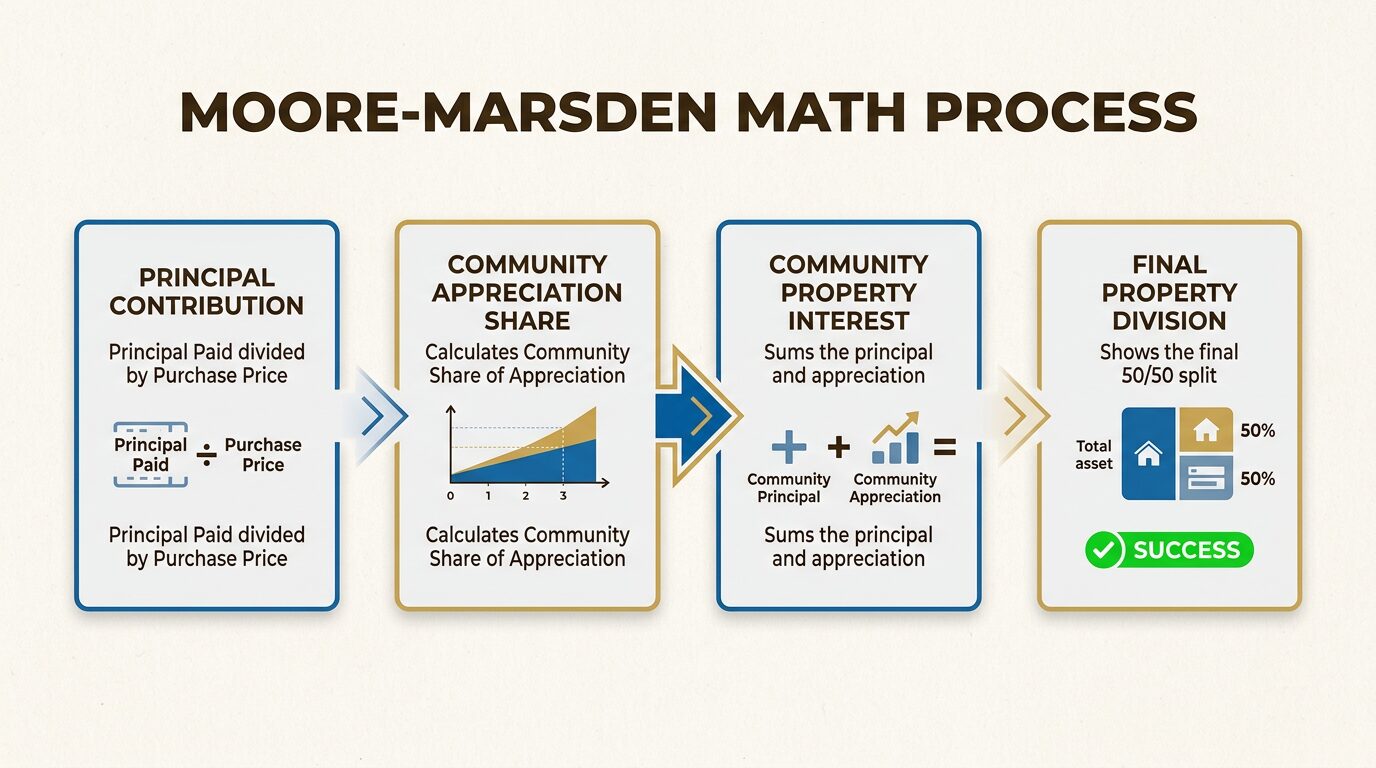

The Moore-Marsden calculation determines the community’s pro tanto (proportional) interest by dividing principal paid with community funds by the original purchase price, then applies that percentage to the total appreciation during marriage.

Let’s break down the calculation step by step:

Step 1: Calculate the community’s pro tanto interest

Divide the principal paid with community funds by the original purchase price:

Principal paid with community funds ÷ Original purchase price = Community percentage

Step 2: Calculate the community’s share of appreciation

Multiply the community percentage by the total appreciation during marriage:

Community percentage × Total appreciation during marriage = Community share of appreciation

Step 3: Determine total community interest

Add the principal paid down to the community’s share of appreciation:

Principal paid down + Share of appreciation = Total community interest

Step 4: Split between spouses

The total community interest is divided equally (50/50) between both spouses:

Total community interest ÷ 2 = Each spouse's share

Example calculation

Consider a typical Los Angeles scenario:

| Component | Amount |

|---|---|

| Original purchase price (2017) | $800,000 |

| Mortgage balance at marriage | $600,000 |

| Principal paid during marriage | $120,000 |

| Community pro tanto percentage | 15% ($120,000 ÷ $800,000) |

| Property value at separation (2024) | $1,300,000 |

| Appreciation during marriage | $500,000 |

| Community share of appreciation | $75,000 (15% × $500,000) |

| Total community interest | $195,000 |

| Each spouse receives | $97,500 |

In this example, the purchasing spouse keeps their separate property interest plus half the community interest, while the non-purchasing spouse receives $97,500. The exact amounts depend on accurate valuations at both the date of marriage and the date of separation or trial.

This type of precise calculation is why working with an experienced Los Angeles divorce attorney matters. Small errors in valuation or calculation methodology can shift tens or hundreds of thousands of dollars between spouses.

What complications arise in high-value Los Angeles properties?

High-net-worth divorces in Los Angeles introduce complications including multiple properties, significant appreciation, refinancing, home improvements, and tracing issues that require forensic accounting expertise.

Los Angeles real estate presents unique challenges for Moore-Marsden calculations:

Substantial appreciation: LA properties often appreciate hundreds of thousands or millions of dollars during a marriage. A small percentage difference in the calculation can equal six or seven figures.

Refinancing complications: Many couples refinance during marriage to take advantage of lower rates or extract equity. Refinancing can change the character of the debt and potentially transmute separate property into community property, especially if the title is changed to include both spouses.

Home improvements: Community-funded renovations complicate appreciation calculations. Determining how much value increase stems from improvements versus market appreciation requires careful analysis.

Multiple properties: High-net-worth couples often own vacation homes, investment properties, or rental units. Each property requires its own Moore-Marsden analysis.

Documentation challenges: Historical valuations, mortgage statements, and improvement receipts may be difficult to obtain, especially for properties owned for decades.

Navigating the Los Angeles County Superior Court system

In our practice, we’ve found that LA County Superior Court judges at the Stanley Mosk Courthouse and other family law centers expect precise calculations and expert testimony for high-value properties. The court maintains a complex case management system, and complex property division matters often require multiple hearings and extensive documentation.

Local judges are familiar with Moore-Marsden principles but rely on attorneys to present accurate calculations supported by credible expert testimony. When hundreds of thousands of dollars hang in the balance, forensic accountants and real estate appraisers become essential members of the legal team.

What are the most common Moore-Marsden mistakes to avoid?

Common errors include confusing interest with principal payments, overlooking appreciation, relying on estimates instead of appraisals, ignoring refinancing impacts, and attempting DIY calculations without legal guidance.

In our experience handling high-net-worth divorces, we see the same mistakes repeatedly:

Confusing interest with principal: Only the portion of mortgage payments that reduces the loan principal affects the Moore-Marsden calculation. Interest, property taxes, and insurance do not count, even when paid with community funds. Many people overestimate their community share by mistakenly including these expenses.

Overlooking appreciation: The community is entitled to a proportional share of the home’s appreciation during the marriage, not just the principal paid down. Failing to include appreciation can drastically undervalue the community’s interest.

Using estimates instead of professional appraisals: Online valuation tools and tax assessments do not reflect accurate market valuations. Courts require appraisals from qualified professionals who can provide credible, defensible estimates of fair market value at specific dates.

Ignoring title changes: Adding a spouse to the property title may transmute separate property into community property, fundamentally changing the analysis. This is often done during refinancing without understanding the legal consequences.

Attempting DIY calculations: Moore-Marsden calculations require precise numbers, accurate tracing of funds, and understanding of complex legal principles. Well-meaning errors can cause long-term financial harm.

Poor documentation: Missing mortgage statements, improvement receipts, or historical valuations force courts to make assumptions that may not reflect the true financial history.

This complex process is exactly how we approach cases at The Marsh Firm to ensure no detail is overlooked. Our network includes trusted forensic accountants and valuation experts who specialize in high-net-worth property division. When hundreds of thousands of dollars are at stake, precision matters. If you are facing this challenge, you can request a private consultation today to get started with expert legal guidance tailored to your situation.

How does Moore-Marsden interact with other property division issues?

Moore-Marsden calculations often intersect with 2640 reimbursement claims, separate property tracing, spousal support considerations, and child custody decisions about the family home.

The Moore-Marsden formula rarely exists in isolation. It intersects with several other property division concepts:

2640 reimbursements: When separate property funds are used for community property expenses (or vice versa), Family Code Section 2640 may allow reimbursement claims. These can run parallel to Moore-Marsden calculations.

Separate property tracing: Tracing separate funds used for improvements or mortgage paydown requires detailed financial records. The burden of proving separate property claims falls on the spouse making the claim.

Family home preservation: When children are involved, courts may order a deferred sale of the family home under Family Code Sections 3800-3810. This allows children to remain in the home for a specified period, with sale deferred until a triggering event occurs.

Offset agreements: Rather than selling the home, one spouse may keep the property while the other receives equivalent assets. Accurate Moore-Marsden calculations are essential for fair offsets.

Tax implications: Capital gains considerations, mortgage interest deductions, and property tax basis adjustments all factor into the overall financial picture.

Child custody considerations often influence how Moore-Marsden interests are handled in practice. Parents may negotiate buyouts or deferred sales to minimize disruption to children’s lives, even when strict financial calculations might suggest a different approach.

What should you do if Moore-Marsden applies to your divorce?

Gather all documentation immediately, obtain professional appraisals, consult an experienced family law attorney, and consider working with forensic accountants to ensure accurate calculations.

If you believe the Moore-Marsden formula applies to your situation, take these steps:

Document everything: Collect mortgage statements from the date of marriage to present, receipts for any improvements made during the marriage, purchase documents, and records of any refinancing or title changes.

Get professional appraisals: Obtain appraisals from qualified professionals for both the date of marriage and current value. Historical appraisals may require specialists who can reconstruct value based on market conditions at that time.

Hire experienced counsel: Not all family law attorneys understand complex property division. Look for attorneys with specific experience in high-asset divorces and Moore-Marsden calculations.

Consider mediation: Negotiated settlements often produce better outcomes than litigation. Mediation allows creative solutions that courts cannot impose.

Act quickly: Delay can mean lost documents, disputed valuations, and deteriorating negotiating positions. The sooner you begin gathering information, the stronger your position.

Next steps: protecting your interests in a Los Angeles divorce

At The Marsh Firm, we understand that your home represents more than equity. It represents stability, memories, and your family’s future. Our approach combines precise legal analysis with strategic negotiation to achieve outcomes that protect what matters most.

We’ve guided high-net-worth clients through complex property divisions involving multi-million dollar estates, multiple properties, and intricate financial structures. Our network includes forensic accountants, real estate appraisers, and valuation experts who understand the nuances of high-asset divorce in Los Angeles.

The Moore-Marsden formula is just one tool in a complex property division. The attorneys who fare best are those who understand both the technical calculations and the strategic opportunities for negotiation. We focus on achieving resolutions that serve your long-term interests rather than prolonging conflict.

If you are facing a divorce involving complex property division, you can request a private consultation today to get started with expert legal guidance tailored to your situation. We’ll help you understand your rights, evaluate your options, and develop a strategy that protects what you’ve worked to build.

Frequently Asked Questions

Who gets the house in a California divorce if one spouse bought it before marriage?

The purchasing spouse generally retains their separate property interest, but the non-purchasing spouse may be entitled to a share of the equity through the Moore-Marsden formula if community funds paid down the mortgage during the marriage. The exact division depends on the principal paid down, appreciation during the marriage, and other factors.

What is the difference between community property and separate property in California?

Community property includes assets acquired during marriage, which are divided equally in divorce. Separate property includes assets owned before marriage, gifts, inheritances, and property acquired after separation. The Moore-Marsden formula addresses the hybrid situation where a separate property home acquires community property characteristics through mortgage payments.

Does refinancing affect Moore-Marsden calculations?

Refinancing can significantly complicate Moore-Marsden calculations. If the refinance changes the title to include both spouses, the property may be transmuted into community property. Even without a title change, refinancing can alter the character of the debt and affect tracing of principal payments.

How is home appreciation divided in a California divorce?

Under the Moore-Marsden formula, the community receives a proportional share of appreciation based on the ratio of community principal payments to the original purchase price. If community funds paid 15% of the original purchase price in principal, the community receives 15% of the appreciation during the marriage.

Do I need a forensic accountant for my Moore-Marsden calculation?

For high-value properties or complex financial situations, a forensic accountant is highly recommended. They can trace funds, verify calculations, and provide expert testimony if needed. The cost of professional analysis is often small compared to the financial stakes involved.