What Happens to Your 401k in a Divorce in California: How Courts Divide Retirement Accounts in Los Angeles

What Happens to Your 401k in a Divorce?

The short answer is this: when you divorce in California, any contributions made to retirement accounts during your marriage are considered community property and will be divided equally between you and your spouse. This is true regardless of whose name is on the account.

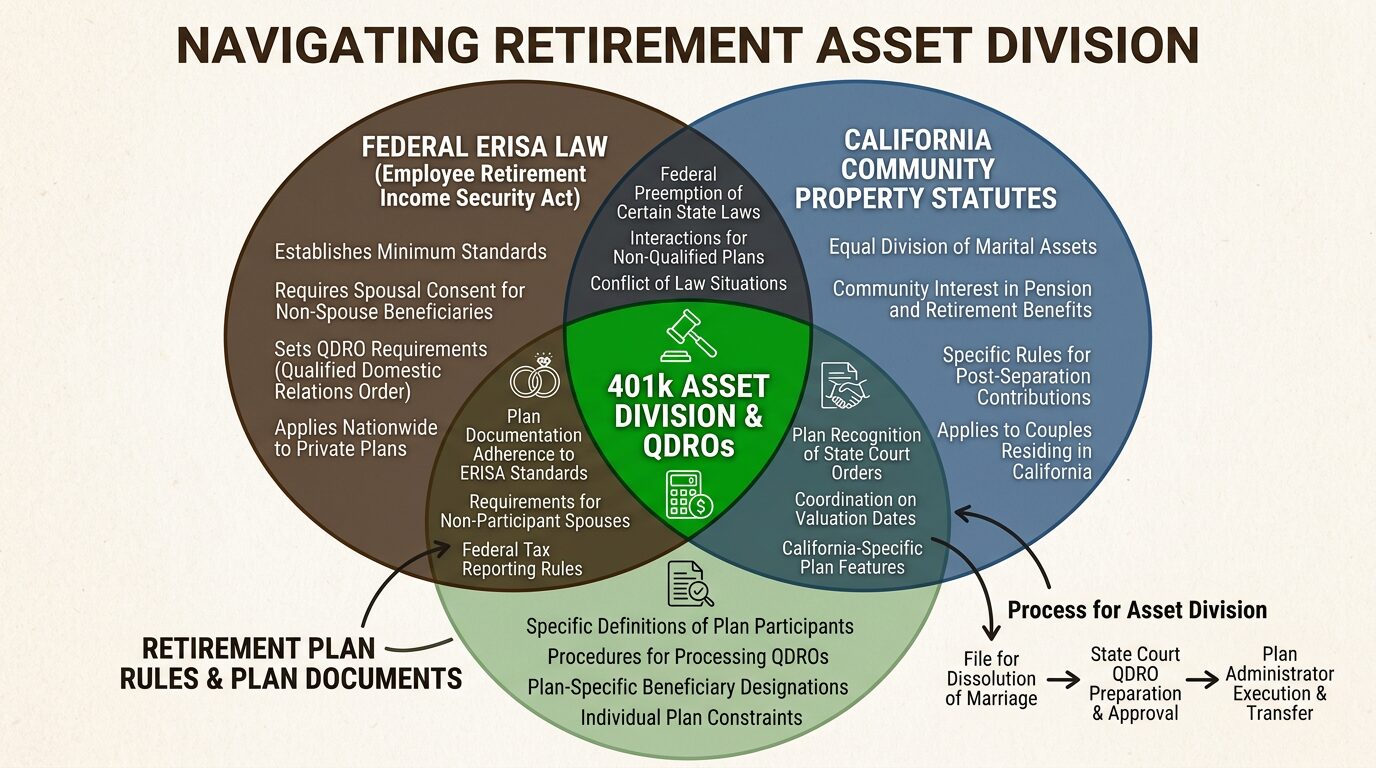

But the actual process is more complicated than simply splitting a balance in half. Federal law, state law, and the specific rules of your retirement plan all intersect here. A mistake in how your retirement accounts are handled can cost you thousands in taxes and penalties, or leave you with less than you are entitled to receive.

This guide explains how 401k and retirement account division works in California, what a QDRO is and why it matters, and how to protect your financial future through the divorce process.

What is a QDRO and Why Do You Need One When Dividing Retirement Assets in a California Divorce?

A Qualified Domestic Relations Order, or QDRO, is a court order that allows retirement plan administrators to divide certain types of retirement accounts between divorcing spouses without triggering tax penalties or early withdrawal fees. Think of it as a legal permission slip that tells your 401k or pension plan administrator exactly how to split your retirement benefits.

Without a properly drafted and approved QDRO, the plan administrator cannot legally transfer funds to your ex-spouse. Attempting to divide the account without one can result in immediate taxation, early withdrawal penalties of 10 percent if you are under age 59½, and the loss of significant value.

Retirement Accounts in Los Angeles Divorce That Require a QDRO vs. Those That Do Not

Not all retirement accounts follow the same rules. Understanding which accounts require a QDRO and which do not is essential to avoiding costly mistakes.

| Account Type | QDRO Required? | How It Is Divided |

|---|---|---|

| 401(k) plans | Yes | QDRO directs plan administrator to transfer marital portion |

| 403(b) plans | Yes | Same process as 401(k) |

| Pension plans / Defined benefit | Yes | Time rule formula calculates marital share |

| Profit-sharing plans | Yes | QDRO required for distribution |

| Employee Stock Ownership Plans | Yes | QDRO directs share transfer |

| Traditional IRA | No | Transfer incident to divorce under IRC Section 408(d)(6) |

| Roth IRA | No | Same transfer process as Traditional IRA |

| CalPERS | DRO required | California Public Employees use Domestic Relations Order |

| CalSTRS | DRO required | Teachers’ retirement system has specific procedures |

| Military retirement | USFSPA order | Uniformed Services Former Spouses’ Protection Act |

IRAs are the exception. They do not require a QDRO. Instead, they are divided through a transfer incident to divorce, which must be clearly stated in the divorce judgment. When done properly, the transfer allows funds to move from one spouse’s IRA to the other without triggering taxes or early withdrawal penalties. However, if the transfer is handled incorrectly, it may result in immediate taxation and penalties.

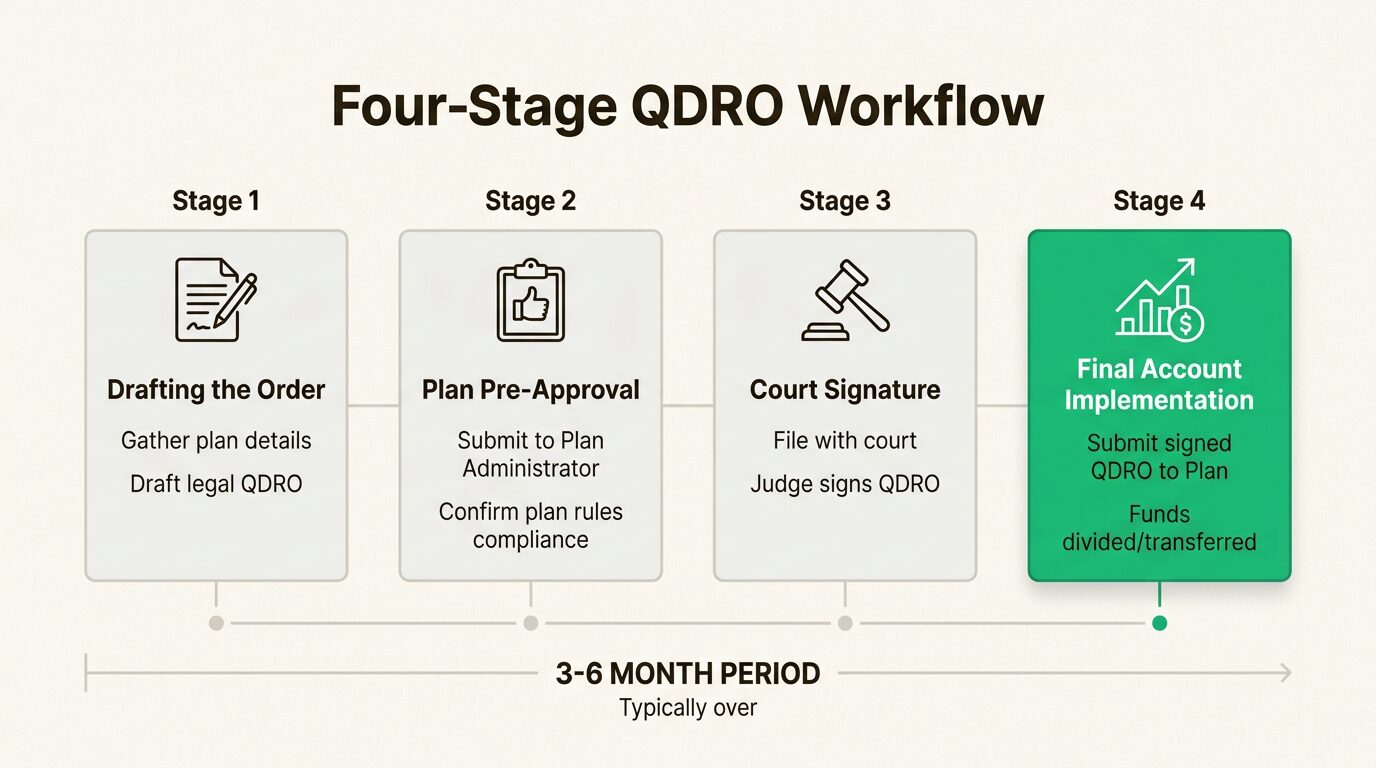

The Timeline for Dividing Retirement Assets California Divorce

The timeline for dividing a 401k or other retirement account typically spans three to six months from the date your divorce is finalized. This surprises many clients who assume the division happens automatically when the divorce decree is signed. It does not. The QDRO is a separate legal document that must be prepared, approved, and implemented after the divorce is complete.

Here is a realistic breakdown of the timeline:

QDRO drafting: Two to four weeks. An attorney or QDRO specialist prepares the order using your specific plan’s language and requirements.

Plan administrator pre-approval: Thirty to sixty days. Most attorneys send a draft to the retirement plan administrator for informal review before submitting to the court. This step catches errors that would otherwise cause rejection later. Plan administrators may charge review fees ranging from $300 to $800.

Court filing and signature: Two to four weeks. Once the plan administrator approves the draft language, the document is filed with the divorce court for the judge’s signature.

Final implementation: Two to four weeks. After the judge signs, certified copies go to the plan administrator, who then divides the account according to the QDRO terms.

Delays happen. Plan administrators have backlogs. Drafting errors require revisions. Missing documentation stalls the process. In our experience, the clients who stay organized and responsive move through this process faster than those who treat the QDRO as an afterthought.

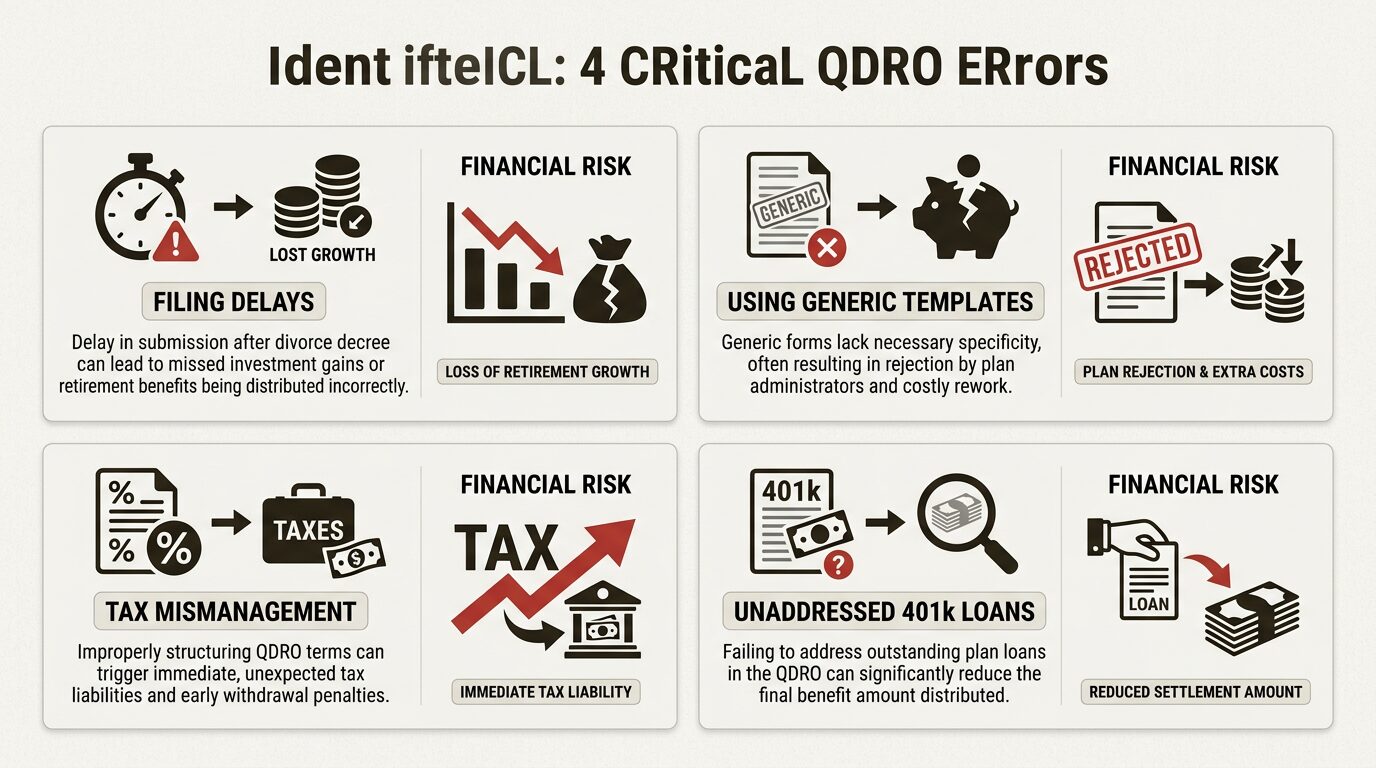

Common and Costly Mistakes When Dividing Retirement Assets

Mistakes involving retirement accounts are common, and they are often expensive. Because retirement assets are designed to grow over time, even small errors can compound and significantly affect your financial future.

Waiting too long to file the QDRO

Your divorce decree establishes your legal right to a portion of the retirement benefits, but you do not actually receive those benefits until the QDRO is completed and implemented by the plan administrator. This gap between divorce finalization and QDRO completion creates real risk.

The employee spouse might die, remarry, or change jobs, potentially complicating or eliminating the non-employee spouse’s rights. If the participant spouse retires and begins taking distributions before the QDRO is in place, recovering your share becomes significantly more difficult. There is no strict statute of limitations for filing a QDRO in California, but practical deadlines exist. The longer you wait, the harder it becomes to locate plan administrators, obtain necessary documents, and coordinate with an ex-spouse who may be less cooperative than during the divorce.

Using generic templates or inexperienced preparers

Many people attempt to save money by using generic QDRO templates found online or through document preparation services. These templates rarely account for the specific requirements of individual retirement plans and often contain language that causes plan administrators to reject the orders.

Each retirement plan has its own model QDRO language and administrative requirements. A 401k plan at a major technology company has different procedures than a pension plan at a government agency. The cost of correcting a defective QDRO often exceeds the expense of having it prepared correctly from the beginning.

Ignoring tax implications

QDRO transfers themselves are not taxable events. But what you do with the funds after transfer matters enormously. If the alternate payee chooses immediate cash distribution, they will generally be subject to income tax on the amount received. While the 10 percent early withdrawal penalty is usually waived for QDRO distributions, the income tax liability remains.

Rolling the QDRO distribution to an IRA preserves the tax-deferred status and provides more investment options than most employer plans. The rollover must be completed properly to avoid tax consequences. We have seen clients lose thousands to unnecessary taxation because they did not understand the difference between a direct rollover and a cash distribution.

Failing to address loans against the 401k

Outstanding loans against a 401k complicate division. Some plans require the loan to be paid off before any distribution can occur. Others may offset the loan balance against the alternate payee’s share. The QDRO should specifically address how any outstanding loans will be handled to avoid surprises.

Special considerations for high-net-worth divorces

For high-net-worth individuals, retirement account division often involves complexities that go beyond the standard QDRO process. At The Marsh Firm, we regularly handle cases involving multiple retirement accounts, executive compensation plans, and sophisticated asset structures.

Multiple retirement accounts across employers

Executives and professionals who have changed jobs multiple times may have retirement accounts scattered across several former employers. Each account requires its own QDRO. Coordinating these multiple orders, each with different plan administrators and procedures, requires careful project management. Missing one account in the divorce settlement can leave significant assets undivided.

Executive compensation plans, including deferred compensation arrangements and supplemental executive retirement plans, often fall outside standard ERISA rules. These plans may require specialized orders or different division strategies altogether, involving complex valuation issues and tax planning considerations.

Defined benefit pensions vs. defined contribution plans

Defined contribution plans like 401ks have a current account balance that is relatively straightforward to divide. Defined benefit pensions are more complicated. They promise future monthly payments, often beginning at retirement age, rather than having a current balance.

California courts typically use a time rule formula to determine what portion of a pension is community property. This formula compares the total length of the employee’s service against the number of years the employee worked during the marriage. The resulting percentage represents the community’s share of the pension.

Rather than receiving an immediate payout, the non-employee spouse usually receives their share when the pension begins paying benefits in the future. Survivor benefits must be specifically addressed in the QDRO language. If the employee spouse dies before retirement, the alternate payee may lose their rights to any benefits unless survivor coverage is properly assigned.

Navigating the Los Angeles County process

For divorces filed in Los Angeles County, the QDRO process follows California state law with local procedural variations. The LA County Superior Court handles QDRO approvals as routine administrative matters when both parties agree to the terms, meaning you typically will not need a court hearing.

Los Angeles has a significant concentration of entertainment industry and technology sector employers, each with unique retirement plan structures. Union pension plans in the entertainment industry, for example, often have specific procedures for dividing benefits that differ from standard corporate 401k plans. Tech companies may offer complex equity compensation structures that interact with retirement planning.

Working with a family law attorney who understands these local nuances matters. At The Marsh Firm, we maintain relationships with forensic accountants and valuation experts in Los Angeles who can address complex retirement account valuations when necessary. We also coordinate with QDRO specialists who understand the specific requirements of major local employers.

Protecting your financial future after divorce

Once your retirement accounts are divided, your work is not finished. Several steps can help protect your long-term financial security.

Update beneficiary designations. Divorce does not automatically remove your ex-spouse as the beneficiary of your retirement accounts. You must complete new beneficiary designation forms with each plan administrator. Failing to do this can result in your ex-spouse receiving your retirement benefits if you die.

Consider catch-up contributions. If you are over age 50, you can make additional catch-up contributions to your retirement accounts. For 2026, the catch-up contribution limit for 401k plans is $7,500 above the standard limit. If your retirement savings were significantly reduced by the divorce, maximizing these contributions can help rebuild your nest egg.

Reassess your retirement timeline. Losing half of your marital retirement assets may require adjusting your retirement plans. Some people choose to work longer. Others adjust their expected retirement lifestyle. Understanding the impact of the division on your long-term financial picture allows you to make informed decisions.

Coordinate with financial and tax professionals. The division of retirement accounts has immediate tax implications and long-term financial planning consequences. Working with a financial advisor who understands divorce-related retirement issues can help you make smart decisions about rollovers, investments, and future contributions.

This complex process, with its overlapping federal regulations, state community property laws, and plan-specific requirements, is exactly how we approach cases at The Marsh Firm. We ensure no detail is overlooked, from identifying all retirement assets to drafting QDROs that actually get approved. If you are facing this challenge, you can request a private consultation today to get started with expert legal guidance tailored to your situation.

Request a consultation to discuss your retirement division

Dividing retirement accounts in a California divorce requires precision, patience, and attention to detail. The difference between a properly handled division and a botched one can amount to tens of thousands of dollars, not to mention years of financial stress.

At The Marsh Firm, we represent high-net-worth individuals and professionals navigating complex property division in Los Angeles and surrounding communities. We understand that retirement accounts often represent decades of careful saving, and we approach their division with the seriousness it deserves.

If you have questions about how your 401k, pension, or other retirement accounts will be divided in your divorce, we can help. Our team will review your specific situation, explain your rights under California law, and develop a strategy to protect your financial future.

Contact The Marsh Firm today to schedule a confidential consultation and learn how we can assist with your retirement account division and other complex property matters.

Frequently Asked Questions About What Happens to Your 401k in Divorce in California

Do I get half of my spouse’s 401k in a California divorce?

You are entitled to half of the portion of the 401k that was contributed during your marriage. Contributions made before marriage or after separation remain the separate property of the account holder.

How long do I have to be married to get a share of my spouse’s 401k?

There is no minimum marriage duration required. Even a short marriage of one or two years creates community property rights to retirement contributions made during that time.

Can my ex-spouse claim my 401k years after our divorce is final?

If the divorce judgment awarded your ex-spouse a share of your 401k but the QDRO was never completed, they may still be able to pursue their portion.

What happens if my spouse cashes out their 401k during our divorce?

California’s Automatic Temporary Restraining Orders prohibit either spouse from withdrawing retirement funds without consent. The court can impose sanctions including awarding you 100 percent of the community interest.

Do I pay taxes when I receive my share of my spouse’s 401k?

If the transfer is done correctly through a QDRO and you roll the funds into an IRA, there are no immediate taxes or penalties. Cash distributions will owe income tax.

What is the difference between a QDRO and a DRO?

A QDRO applies to private employer retirement plans governed by ERISA. A DRO is used for government retirement systems like CalPERS and CalSTRS.